Understanding Net Working Capital for Businesses

Have you ever looked at your sales report, seen a healthy profit, but then felt a knot in your stomach when it was time to pay your suppliers? You’re not alone. This stressful gap between “making money” and “having money” is one of the most common—and confusing—challenges for entrepreneurs, stemming from a simple truth: profit on paper is not the same as cash in the bank.

But what if a single number could act as a pulse check on your business’s short-term health? This metric answers the critical question, “Do I have enough cash to survive a slow month?” and cuts through the confusion about working capital vs cash flow.

That number exists, and it’s called Net Working Capital. Understanding net working capital for businesses provides the financial peace of mind you need to make confident decisions. This guide explains why working capital is important, transforming anxiety into a clear action plan.

What Your Business Can Use Now: A Simple Guide to Current Assets

To understand your financial breathing room, start with your short-term resources, known as Current Assets. These are assets your business owns that can be converted to cash within 12 months, which you can use to pay upcoming bills and fund daily operations.

This includes more than the cash in your bank account. For most small businesses, the list of current assets includes a few key items:

Cash in the bank: The most obvious and most useful asset.

Accounts Receivable: Money owed to you by customers for services or products they’ve already received. Think of these as your outstanding invoices.

Inventory: The value of the products on your shelves or the raw materials you have waiting to be used.

While your invoices and inventory hold value, they aren’t cash. To get the full picture, you must also consider what you owe.

What Your Business Owes Soon: Demystifying Current Liabilities

The other side of the story is what you owe. Your short-term obligations are called Current Liabilities—any debt or bill due within the next 12 months. Think of these as the financial promises you need to keep in the near future.

These obligations are the other key components of working capital. For most businesses, the list is straightforward. The significant role of accounts payable in working capital makes it the most common liability, but there are others:

Accounts Payable: The money you owe to your suppliers for goods or services.

Accrued Expenses: Costs you’ve incurred but haven’t paid yet, like employee wages for the last pay period.

Short-Term Loan Payments: The portion of any loan that is due within the year.

It’s crucial to separate these immediate bills from long-term debt. That five-year business loan you took out isn’t a current liability, but the twelve months of payments you’ll make on it this year are. With a clear view of both what you have and what you owe, you’re ready to find your true financial standing.

How to Calculate Your Financial ‘Safety Cushion’ in 60 Seconds

Now, bring your current assets and liabilities together to see if you have enough to cover upcoming bills. This calculation reveals your financial breathing room.

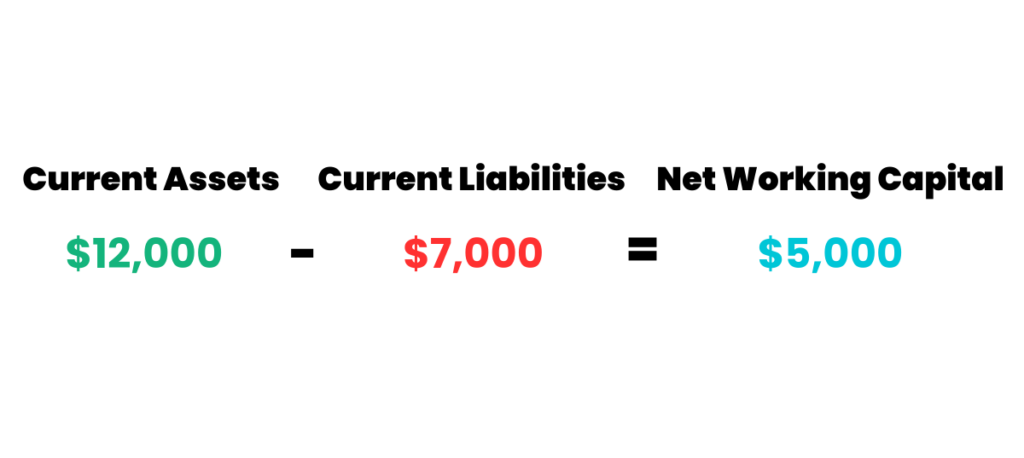

Figuring out your position is surprisingly easy. The net working capital formula involves one simple subtraction:

Net Working Capital = Current Assets – Current Liabilities

Let’s use a simple working capital calculation example. Imagine your business has $10,000 in Current Assets (cash and inventory) and $6,000 in Current Liabilities (supplier bills and payroll). Following the formula, you subtract the $6,000 you owe from the $10,000 you have.

That remaining $4,000 is your Net Working Capital. Think of it as your business’s short-term financial safety net. It’s the cash buffer you have available to handle emergencies, survive a slow sales month, or seize a new opportunity without falling behind on your bills. Having a positive number here is a great sign.

Positive Working Capital: Your Business’s Breathing Room Explained

That positive $4,000 in our example is more than a number; it’s a signal of good short-term financial health. Positive working capital indicates your business has enough resources to cover all upcoming bills with money left over. This position of strength lets you operate confidently instead of worrying about making payroll.

Think of this positive balance as your operational breathing room. If a crucial piece of equipment suddenly breaks or a large client pays their invoice late, you don’t have to panic. This financial cushion provides the flexibility to handle surprises without scrambling for a loan.

This buffer isn’t just for defense, either. Positive working capital empowers you to seize opportunities, like buying inventory in bulk for a discount or investing in a small marketing campaign. It puts you in control. Of course, the story is very different when we consider positive vs negative working capital, which raises an important question: is a negative number always a red flag?

Is Negative Working Capital Always a Red Flag?

A negative result is often a crucial warning. It means your short-term debts are greater than your short-term assets—you owe more money soon than you’ll have available. This can create a stressful cash crunch, and it indicates your financial buffer has disappeared.

However, a negative result isn’t a universal sign of doom. Consider a busy grocery store: they collect cash from customers instantly but might have 30 days to pay their suppliers. This efficient working capital cycle for a small business means they use their suppliers’ money to fund operations. For them, negative NWC is a feature of a healthy, fast-moving business model, not a flaw.

Ultimately, analyzing working capital requires understanding your industry’s unique rhythm. For a service business waiting on a big client payment, negative NWC is a serious risk. For a subscription service getting paid upfront, it can be completely normal. Making this distinction allows you to move from simply calculating a number to making truly confident financial decisions.

From Numbers to Confidence: Your 5-Minute Working Capital Action Plan

To make this real, grab a notepad. On one side, list your current assets (cash, money customers owe you). On the other, list your current liabilities (supplier bills, upcoming payroll). This simple subtraction gives you a snapshot of your operational health.

This number is your starting point for better working capital management. It’s the first step toward turning financial anxiety into confident decision-making.

Using Coast Funding to Strategize with Working Capital Needs

Knowing the health your net working capital outlook is critical for success in business. How much can I afford to invest in product this month? How aggressive can I be in marketing? Can I afford to expand or should I focus on maintenance? These are questions you can answer with knowing your net working capital. Depending on timing, business goals, delayed payments and receivables, and other factors you face while running a business, Coast’s Working Capital Lines and Business Funding Products can help get you where you want to be.

Our experienced funding advisors work with clients every day to ensure their funding strategy matches the needs of their business. Using responsible working capital to your advantage can give your business stability, confidence, and the ability to keep running smoothly.

Take the first step: Apply Here

Read client reviews: Trust Pilot

Business Funding FAQ's

Net working capital is a snapshot of your business’s short-term financial health. It shows whether you have enough near-term resources to cover bills due soon.

Net Working Capital = Current Assets − Current Liabilities

Current assets are resources you can convert to cash within about 12 months, such as:

Cash in the bank

Accounts receivable (unpaid invoices)

Inventory (products/materials you expect to sell/use)

Coast Funding utilizes a soft pull to verify identity and determine qualifications. Applying and seeing what you qualify for will not impact your personal credit score. Certain programs may result in a hard inquiry; however, this will only occur with notice after an approval has been issued and your offer has been accepted. Further, if you default on a Coast Funding program you may be subject to negative business reporting and personal credit reporting where applicable.

Current liabilities are bills and debts due within 12 months, such as:

Accounts payable (supplier bills)

Accrued expenses (like wages you owe)

The next 12 months of loan payments

If timing, receivables delays, growth goals, or seasonal swings are squeezing your buffer, Coast’s working capital lines and business funding products can help bridge gaps and align your funding strategy with how your business actually operates.